Discover Your Money Personality Type

1. The Busy Bee

Money Superpower: Giving your all to your work and your money-making endeavors.

Personal Pitfall: Always putting work and wealth ahead of your relationships and experiences.

Most Likely to: Be one of the hardest working people in any room; do the extra work to get ahead financially.

2. The Saving Squirrel

Money Superpower: Saving money and squirreling away wealth, even if you have no plans on how to spend it.

Personal Pitfall: Letting a fear of "losing" or spending money prevent you from ever really enjoying it.

Most Likely to: Know the best rates, deals, bargains; have the biggest rainy-day fund.

3. The Lavish Lion

Money Superpower: Showing your generosity and treating others and/or yourself to the finer things, even when there's no "occasion."

Personal Pitfall: Giving into lifestyle creep, going overboard, and losing sight of financial options that could be better than spending right now.

Most Likely to: Be the life of the party, take risks, be the best shopping buddy.

4. The Indifferent Iguana

Money Superpower: Not sweating the small stuff financially, not stressing about money, and being resilient to uncertainty.

Personal Pitfall: Not thinking about money when making important decisions or starting to think of money as "evil."

Most Likely to: Think money isn't the key to happiness.

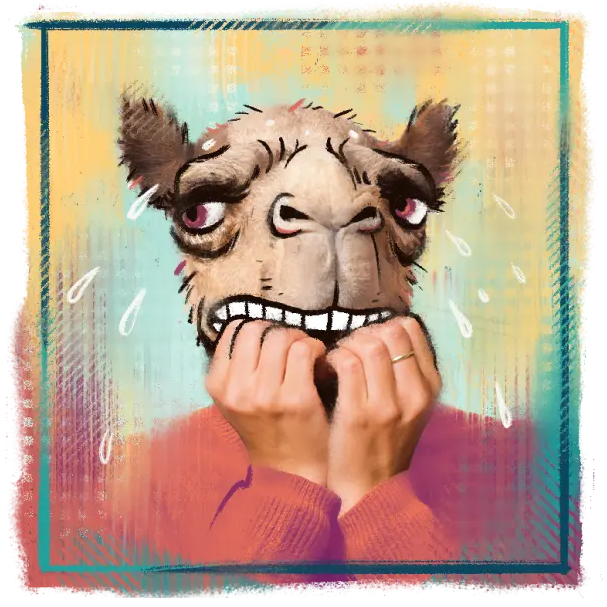

5. The Concerned Camel

Money Superpower: Keeping a close eye on your money and planning for the worst-care scenarios.

Personal Pitfall: Obsessing about losing or running out of money or letting your fears get in the way of opportunities to enjoy life or level-up your wealth.

Most Likely to: Know where the exits are in any room; have a backup plan for the worst-case scenario.

So, what money personality describes you best?

Most of us have money personalities that combine multiple "types."

Whatever yours is, remember there are no "good" or "bad" types. They're all just different. Zeroing in on your types is how you get to know your natural skills and Achilles heels when it comes to finances. That's the only way you can really start to figure out how to improve your financial wellbeing, make better financial choices, and give yourself an even better financial outlook.

Share This Post

OUR LOCATIONS

WEST SIDE OFFICE

Millennium Place East

25111 Country Club Boulevard

Suite 230

North Olmsted, OH 44070

EAST SIDE OFFICE

One Chagrin Highlands

2000 Auburn Drive

Suite 200

Beachwood, OH 44122

CHECK US OUT

The Better Business Bureau membership provides no guaranteed assurance or warranty of the character or competence of the member. BBB charges a fee for BBB Accreditation. Always make financial decisions on the basis of your own due diligence.

Advisory services offered through CreativeOne Wealth, a Registered Investment Adviser. Preservation Retirement Services and CreativeOne Wealth are not affiliated. The insurance products offered by Preservation Retirement Services are not subject to Investment Advisor requirements. The Retirement Protection Plan is our proprietary process name and it does not promise or guarantee investment results or preservation of principal. 2023/07/28 - 17149121